Physical Address

Sydney, Australia 2564

Physical Address

Sydney, Australia 2564

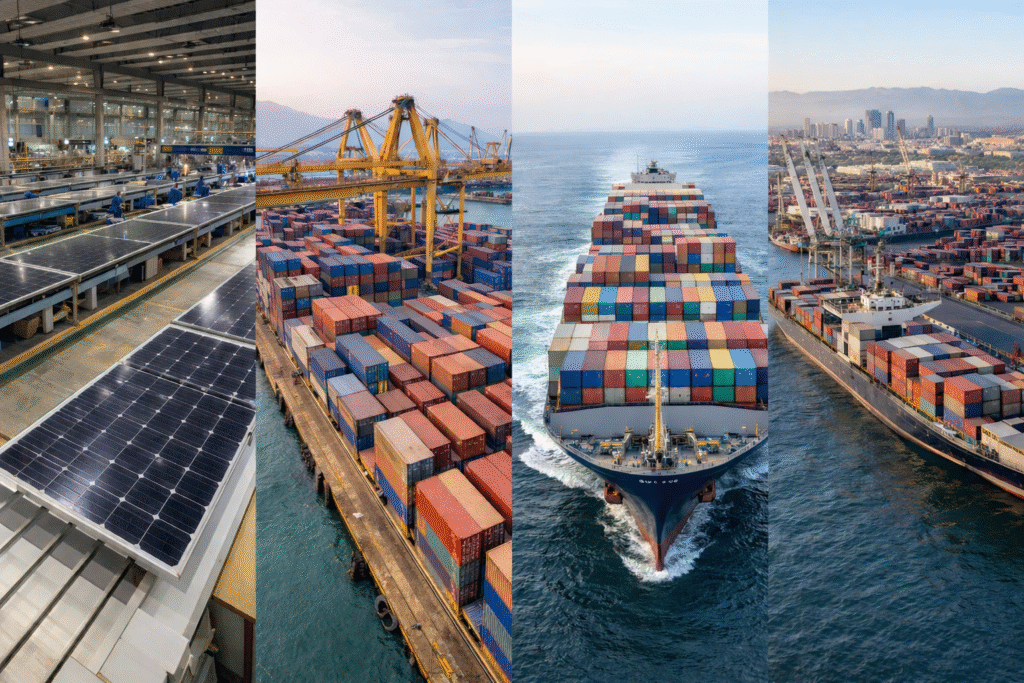

India is quietly emerging as a key solar module supplier to the United States. As trade policies reshape global supply chains, the numbers reveal a deeper shift underway.

India’s position in the global solar supply chain is changing rapidly, driven less by headlines and more by numbers. Over the past two years, the United States has emerged as the dominant destination for Indian-made solar modules, absorbing nearly 97% of India’s solar exports between FY2023 and FY2025, according to industry estimates cited by PL Capital.

This shift coincides with a broader restructuring of US solar imports. As Washington tightened restrictions on Chinese-linked supply chains, US developers were forced to diversify sourcing. India, with expanding manufacturing capacity and competitive pricing, has become one of the key beneficiaries of that transition.

India’s solar module exports rose almost ninefold in 2023, before doubling again in 2024, marking one of the fastest export expansions in the country’s renewable energy sector. While global solar demand has continued to grow, the concentration of Indian exports toward the US reflects policy alignment as much as market forces.

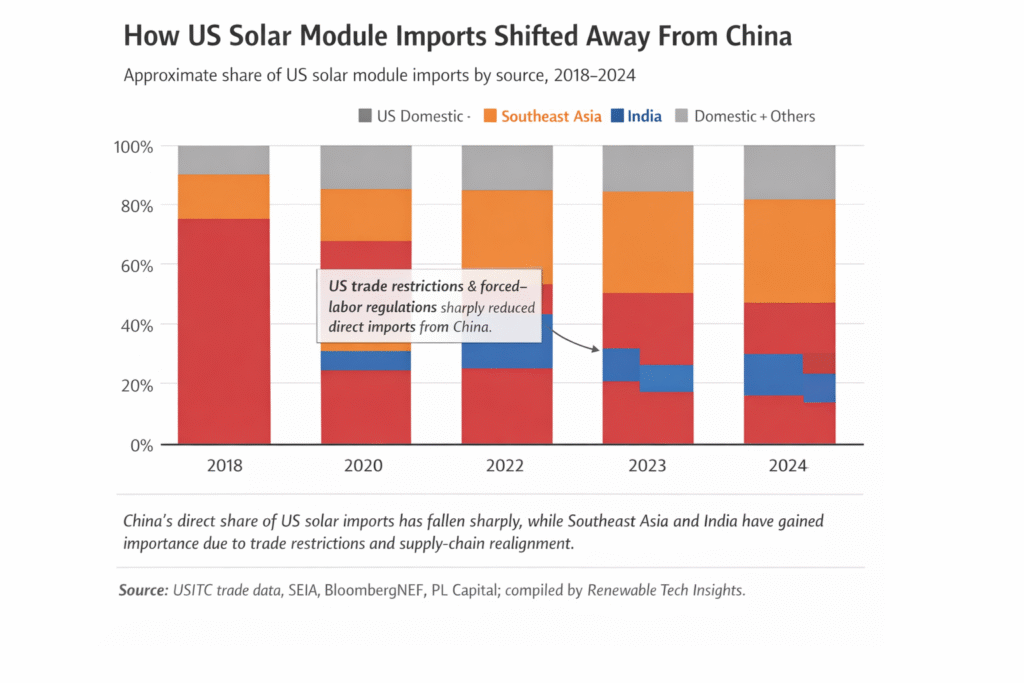

Cost competitiveness remains a critical factor. Indian modules are estimated to be 19–21% cheaper than those manufactured in the US, offering developers a clear cost advantage in a market where utility-scale solar projects remain highly price sensitive. This has helped India expand its share of US solar imports from roughly 3% in 2022 to around 10–12% by 2024. The shift is visible in US import data, which shows how China’s direct share has collapsed while India and Southeast Asia have gained importance.

However, India operates within a competitive landscape. Southeast Asian manufacturers, particularly Vietnam and Malaysia, still dominate US solar imports, accounting for well over half of total supply. Vietnam alone has maintained a share of more than 30% in recent years, largely due to its established manufacturing base and historical role as an intermediary supplier.

The timing of India’s export surge also aligns with rapid growth in US solar deployment. In 2024, the US added approximately 50 GW of new solar capacity, one of its largest annual additions on record. Federal incentives and state-level policies continue to support deployment, sustaining demand even as domestic manufacturing expands.

At the same time, the US has made clear its intention to rebuild local solar manufacturing. This dual objective, scaling installations while reducing reliance on foreign supply chains, has created a complex trade environment for exporters.

Despite recent success, Indian exporters face growing uncertainty. US authorities are investigating allegations of dumping, with provisional margin estimates reportedly exceeding 100%. In parallel, a new tariff framework scheduled for 2026 could raise duties on Indian imports, potentially affecting price competitiveness.

These measures reflect broader geopolitical considerations rather than sector-specific issues alone. As a result, Indian manufacturers must balance short-term export growth with long-term exposure to trade policy shifts.

India is simultaneously scaling up production to meet both domestic and global demand. Total power generation capacity has increased from around 356 GW in 2019 to nearly 475 GW in 2025, driven primarily by renewable energy additions. Solar now represents more than 20% of installed capacity, and is expected to remain the dominant contributor toward India’s target of over 400 GW of renewable capacity by 2030.

Module manufacturing capacity is projected to reach 150–180 GW by the end of the decade, supported by government incentives aimed at strengthening domestic supply chains. This expansion gives India greater flexibility, but also raises questions about how much output will ultimately be absorbed at home versus exported.

India’s growing role in supplying solar modules to the United States reflects a policy-driven reallocation, not a displacement of China’s global dominance. China still accounts for over 70% of global solar module manufacturing, but its direct access to the US market has largely collapsed due to tariffs, forced-labour regulations, and supply-chain scrutiny.

Before these measures, China supplied more than half of US solar module imports. By 2024, that share had fallen to low single digits, with much of the remaining Chinese-linked supply rerouted through Southeast Asia. Even those routes are now narrowing, as US investigations increasingly target circumvention via Vietnam, Malaysia, and Thailand.

India’s current 10–12% share of US solar imports remains modest in global terms, but strategically important. Unlike Southeast Asia, Indian supply chains are viewed as lower regulatory risk, making Indian modules attractive despite not being the lowest-cost option globally.

Looking ahead, even if India reaches 150–180 GW of manufacturing capacity by 2030, only a fraction is likely to be exported. However, allocating just 10–15% of output to markets like the US would meaningfully reduce American dependence on China-linked modules, not by volume dominance, but through diversification.

The broader signal is clear: solar trade is no longer shaped by cost alone. Regulatory alignment, geopolitical risk, and supply-chain transparency are now central to determining who supplies the world’s fastest-growing solar markets.